Failed attempts before Bitcoin paved the way for its eventual success. Each

attempt contributed valuable lessons to the cryptocurrency ecosystem.

1

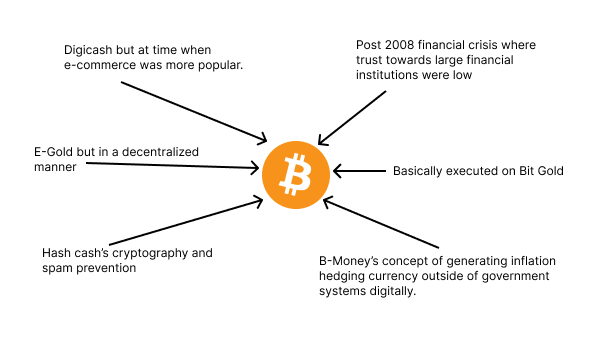

DigiCash by David Chaum (1989)

DigiCash pioneered the concept of digital currency through its Cyberbucks system, which gave new users 100 units of digital money upon registration. This innovative approach to electronic payments emerged in the 1990s as part of DigiCash’s broader mission to revolutionize digital transactions. The system was particularly noteworthy for laying important groundwork in digital payment technology, implementing features like micro-chipped smart cards and secure cryptographic keys that would later become standard in digital wallets and electronic payment systems.Reason for failure: Timing

2

E-gold by Gold and Silver reserves (1996)

Backed by real units of gold and silver. Allowed users instant transfers over the internet. By 2006, there were 3.5 million active e-gold accounts, processing $5.9 million in daily transactions. Innovated micro payments allowing users to pay one ten-thousandth of a gram of gold and developer APIs. Merchants accepted e-gold as form of payment alongside regular credit and debit cards.Reason for failure: Lack of KYC (Know Your Customer protocols), unlicensed money transmission, centralization issue

3

Hash Cash by Adam Back (1997)

Introduced proof of work to verify validity of digital funds. Proof of work computers produce verifiable computationally intensive output for electronic money to have value. Used cryptography (SHA1 encryption). In inception, Back referenced DigiCash, proposed fee for transactions to prevent spam. Would impose economic cost to limit spam. Cryptography solved the double spend problem which enables digital units to be copied like a file and be spent more than once. Used by Microsoft and Apache but never took off.Reason for failure: Not intended for widespread adoption, solved spam issues

4

B-Money by Wei Dai (1998)

B-money introduced the idea of computer science to generate currency outside of governmental systems. Like Hash Cash, he proposed that digital currency would be produced through computation. Digital money would be priced based on other real world assets. Limited in supply to protect against inflation. B-money broadcasted transactions across a network. System would be enforced by digital contracts, which would be used to resolve disputes. Used cryptography instead of centralized authority enabling users of the network to be anonymous. Applied idea of contracts to enforce order to distributed system and proof of work to produce money.Reason for failure: Just a thought experiment

This was more of a thought experiment by Wei Dai to explore the concept of non-governmental money that couldn’t be subject to inflation through a controlled money supply.

5

Economic Climate + Housing Market Bubble (2008)

E-commerce was popular via credit cards, debit cards and PayPal. People wanted a tamper-proof distributed way to send money across the globe and that still hadn’t been created.

Understanding Mortgages and the 2008 Crisis

Understanding Mortgages and the 2008 Crisis

Mortgages: Loans given out to individuals to buy a house.At the beginning of 2006, the world’s financial markets were very strong, economic growth was steady but cracks were beginning to show. The US housing market for the first time was in decline in value as rules in lending were so loose that many borrowers were not able to pay back their obligations.This was disastrous because banks had chopped up these loans and mortgages into private securities that were traded and held like stocks and bonds by financial institutions. When many of those assets turned out to be worthless, it brought on a collapse of the financial system that led to governments around the world to inject cash into the system to save the global economy.Low interest rates led to low returns on government bonds and fixed deposits. It didn’t make sense to buy government bonds or just keep their pile of cash in the bank. So investors wanted to seek out optimal ways to seek alpha (achieving returns higher than a benchmark index or overall market return). They turned to real estate as a vehicle of investment. And since these institutions didn’t want to deal with individual buyers and sellers, they would buy mortgage-backed securities. Basically a bundle of home loans packaged together into a single investment that can be bought and sold. This was a high performing asset class but soon the banks would run out of financially responsible people to lend to. So banks started giving “sub-prime mortgages”, and as the name suggests, they would give these loans out to basically anyone. It soon turned out that these people couldn’t pay back their mortgages and started defaulting their loans. The banks would then take back these houses and put them up for sale. As more and more homes were taken back by the banks and put for sale, the housing market started to tank!

TLDR: The Housing Crisis

- Investors want alpha + low risk

- They turn to real estate

- They didn’t want to buy specific homes

- They bought mortgage-backed securities

- They performed really well

- They wanted more

- Banks were running out of credible debtors to give mortgages to

- They start giving out mortgages like Oprah

- People start defaulting on their mortgages. Banks reclaim homes and list again

- More people start defaulting. Home prices start plummeting

- The mortgage-backed securities were then worth nothing

- Investors lost all their money and were sad